| Fungilble materials |

|---|

Also known as identical or interchangeable materials or accounting segregation provision.

Fungible materials are goods that are identical or interchangeable with the exported good: they have the same technical and physical characteristics and are considered commercially interchangeable.

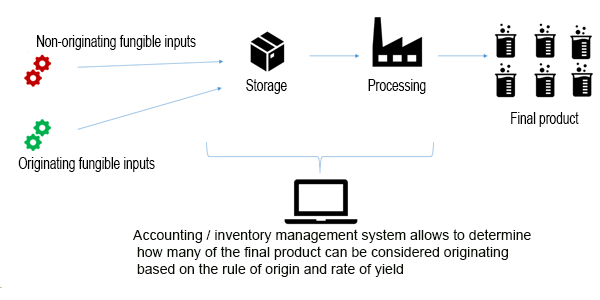

The provision determines how non-originating and originating fungible materials should be tracked (accounted for) when both types are stored together and/or used to produce the final goods. It allows both types of materials to be tracked not through physical identification and separation but based on an accounting or inventory management system.

A company tracks how many originating and non-originating parts it used during a production process and based on this determines the origin of the final product.

Some agreements specify the requirements for the accounting/ management inventory system. Under certain FTAs, using the accounting segregation requires prior authorisation from local customs authorities.

Example:

A product is made from, among other inputs, a type of powder. The producer purchases both originating and non-originating powder. The two types of powder are stored together and the producer cannot track which powder is being used in the production of the final good. Based on the applicable rules of origin, the products made from originating powder meets the origin criteria and the product made from non-originating powder does not. The producer knows how much originating and non-originating materials are stored at a given time and how much powder is used in the production of one unit of the final product. With accounting segregation provision in place, the producer can determine the origin of the final product through the accounting system. Tracking whether the powder used in the production process is originating or not is not required and the origin of the final product is determined based on the overall amount of originating, non-originating materials used in the production on a daily, weekly etc. basis rather than on the precise origin of the inputs that have gone into that product.

Click here for more information on WCO website.

| More Glossary |

|---|